Author: Patti Casaleggio, Invictus Analytics

As regulatory scrutiny and expectations around commercial real estate (CRE) continue to evolve, staying ahead of supervisory trends has never been more critical for community and...

We recently published a post by my partner, Adam Mustafa, noting that AFS bond portfolio losses across the industry reached record levels in the first quarter of 2022. While the increases in interest rates are nowhere near (yet) what we saw in the late 70s-early 80s, or even in the mid-90s, the economic environment has caught a lot of bank CFOs, treasurers, and investment officers flat-footed. That’s because we’re facing a perfect storm of rare conditions:

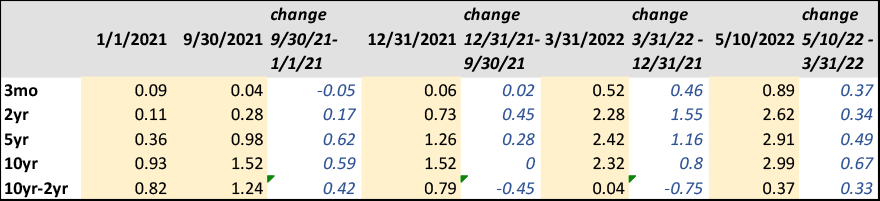

The table below shows that rates rose more in the fourth quarter than they did in the first nine months of the year. But rates have continued to rise from the end of the first quarter of this year through May 10, 2022, in an amount that approximates the increase in the first nine months of 2021.

Source: home.treasury.gov.

Generally, the shorter end of the yield curve is more affected by Fed actions, and the longer end by inflation expectations. In a “normal” (pre-2008 financial crisis) environment, US Treasuries are supposed to provide a positive “real” interest rate (rate less inflation). If inflation continues at 8 percent, then long rates could be (gulp!) greater than 8 percent.

So now what? We’re not in the business of forecasting interest rates but banks that have AFS bond portfolios need to be thinking how they will react to potential scenarios, and what that will mean for their banks, shareholders and regulators. For background, read “How to Spot Risks in Your Investment Portfolio.” Here are three possible scenarios to consider:

In this scenario, Fed rate increases cause a slowdown in inflation. Future rate increases become further spaced out and are potentially 25 basis points instead of 50 basis points. Once inflation is under control, the Fed stops raising rates and then considers lowering them. This is probably a one-to-two-year scenario and is the best outcome for banks. Portfolio hemorrhaging slows down. Bonds roll down the curve as they get closer to maturity. The yield curve stays positively sloped. Deposits run off a bit and become more expensive. Loan portfolios do not show a lot of negative credit migration.

Fed continues to increase rates at a similar pace to what they have recently been doing. Inflation stabilizes but doesn’t decline rapidly. This is a two-to-three-year scenario. Portfolios continue to bleed. The economy starts to slow but remains in a (nominal) growth trajectory. The yield curve stays positively sloped. Deposit runoff is more than in the above scenario and deposit betas increase, causing an increase deposit rates. Net interest margins decline. Positive carry on the investment portfolio declines. Loan portfolios begin to show some bigger problems as interest coverage becomes thinner and asset values do not increase. The higher cost of financing pushes some borrowers out of the market.

The Fed continues to raise rates. Inflation doesn’t abate. The Fed gets more hawkish and aggressive. Short rates rise along with Fed rate increases. The yield curve as defined as 10-year less 2-year stays flat or goes negative. The economy goes into recession. Loan portfolios exhibit larger credit migration problems. Deposits run off as the Fed continues to liquidate its former quantitative easing purchases. Bond portfolios take more losses. This is one-to-three-year scenario and is probably the worst outcome for banks.

There are three more things to remember or to remind your ALCO committee:

As our previous article mentioned, you need to get ahead of regulators on this issue. A well-designed stress test, particularly for a stagflation scenario, along with a liquidity analysis that generates a coherent action plan should be the first step in reigning in the problem.

banking, Capital Plan for Community Banks, Community Banks Capital Plan, capital planning, liquidity, stress testing, Trade War Recession, Capital Requirements for community banks, community bank regulations, Global Oil Shock, Stagflation, Banking CRE, Banking Construction, Concentration Limits, CRE Banking Strategies

Author: Patti Casaleggio, Invictus Analytics

As regulatory scrutiny and expectations around commercial real estate (CRE) continue to evolve, staying ahead of supervisory trends has never been more critical for community and...

banking, Capital Plan for Community Banks, Community Banks Capital Plan, capital planning, liquidity, stress testing, Trade War Recession, Capital Requirements for community banks, community bank regulations, Global Oil Shock, Stagflation

Author: Adam Mustafa CEO, Invictus Analytics

What happens when inflation reaccelerates from already elevated levels while economic growth slows?

This is the defining challenge behind Invictus Analytics’ latest Oil Price Shock...

banking, Capital Plan for Community Banks, Community Banks Capital Plan, capital planning, liquidity, stress testing, Trade War Recession, Capital Requirements for community banks, community bank regulations, cblr

Author: Adam Mustafa, CEO, Invictus Analytics

Federal banking agencies recently finalized a rule lowering the Community Bank Leverage Ratio (CBLR) threshold from 9% to 8%, effective July 1, 2026. At first glance, the change...